As the global economic fallout from the US-Israeli war on Iran continues to mount, the conflict is creating the largest oil supply disruption in history, driving extreme energy market volatility and threatening to upend global trade, inflation dynamics, and economic growth.

Brent crude, which had been trading at around $82 a barrel before the war, climbed to more than $108 on 9 March, crossing the $100 threshold for the first time in nearly four years. During trading, it briefly neared $120, driven by a historic disruption to regional oil production, the invocation of force majeure by several Gulf states on oil and gas shipments, and the broader fraying of supply chains.

As of 13 March, Brent crude was trading above $100 a barrel. Estimates by the US Energy Information Administration suggest that prices may remain above $95 a barrel over the next two months if geopolitical risks persist.

Natural gas markets, meanwhile, suffered an even harsher jolt. Europe’s TTF gas benchmark jumped to around €70 per megawatt-hour on 9 March—a daily rise of roughly 29%—before easing to between €58 and €60 following the European Commission’s announcement that storage levels stood at a secure 65%. The UK, in contrast, with its wafer-thin strategic reserve cushion, saw prices rise by 70%. Prices in Asia rose on the JKM benchmark amid fears of disruption to Gulf liquefied natural gas (LNG) cargoes and the diversion of some shipments away from the region.

According to Goldman Sachs, continued shipping disruptions and supply outages throughout March could push oil prices well beyond $100, with the possibility of reaching $150 a barrel. Market estimates further suggest that between eight and nine million barrels a day of oil supplies could be placed at risk if the war expands.

Financial markets were swift to register the military escalation, translating it into sharp volatility across global trading. As war erupted, bringing with it a convergence of fears over surging oil prices and the prospect of a wider conflict, investors began to reassess inflation and global growth expectations, while geopolitical risk was repriced across asset classes. A broad sell-off in higher-risk assets soon followed, accompanied by an increasingly pronounced flight towards safe havens.

Sharp fluctuations

Against this unsettled backdrop, global equity markets saw sharp fluctuations as tensions intensified. Major indices in the US and Europe fell by 1-2%, while some Asian markets recorded steeper losses. Japan’s Nikkei index shed more than 7% in a single session, while Hong Kong’s Hang Seng declined by around 3%.

In contrast, shares in defence and energy companies such as ExxonMobil and Lockheed Martin posted notable gains, buoyed by expectations of higher military spending and rising energy prices. Technology and transport stocks, whose fortunes are closely tied to the rhythms of global trade, came under pressure as investors braced for higher fuel and shipping costs, along with logistical delays, affecting high-value goods such as electronics and microchips due to airspace restrictions and disruptions to maritime shipping.

During the first week of March, a parallel shift in liquidity flows also became evident. Alongside gold and US government bonds, long regarded as the preferred refuge in moments of major geopolitical crisis, some investors also turned to Bitcoin, often described as ‘digital gold’.

Yet Bitcoin behaved more like a high-risk asset than a pure safe haven, slipping below $68,000 as positions were liquidated to cover equity losses, while gold briefly traded above $5,350 an ounce before retreating amid volatile market conditions.

Blockade efffects

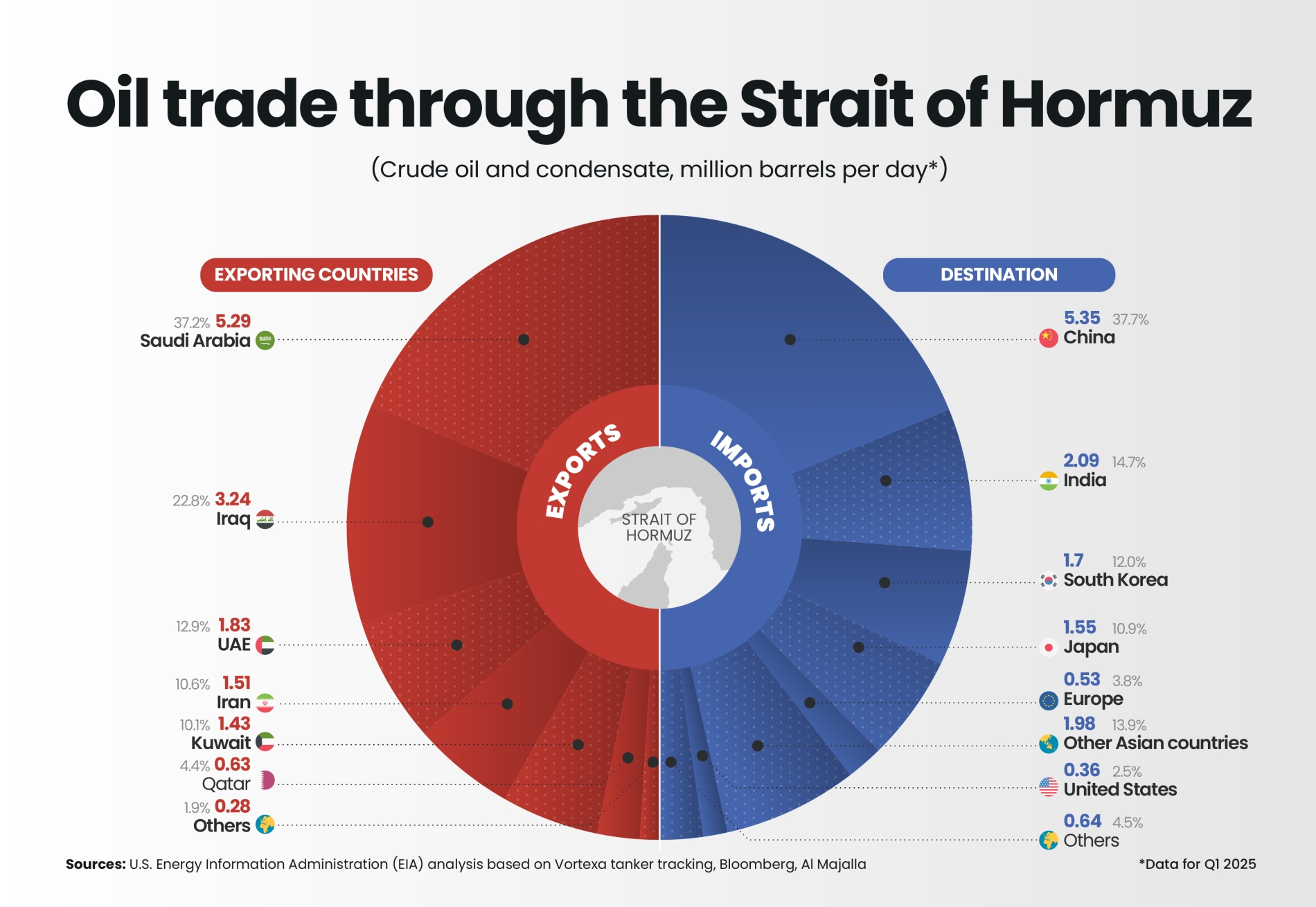

With the world’s attention fixed on the consequences of disrupted oil supplies through the Strait of Hormuz, the blockade may carry longer-term risks for trade flows. With at least 10 vessels attacked in the critical waterway since hostilities began, maritime tracking data shows hundreds of ships lying at anchor on both sides of the strait.

According to shipping industry data, the passage of very large crude oil carriers through the strait has fallen by more than 80%, while around 200 tankers remain stranded in Gulf waters awaiting safe passage.

In the opening days of the conflict, the number of transiting vessels fell from roughly 138 ships a day to only a handful, as most major commercial operators avoided the route. It is likely that most of the vessels still making the crossing are linked to Iran or are operating with their tracking systems switched off under extreme risk conditions.