There are two political clocks running in Beijing this week, and they are not synchronised. Chinese President Xi Jinping's is counting down to the autumn of 2027, when the 21st Party Congress will likely confirm his fourth term but force him to choose a successor, which he has so far refused to do. US President Donald Trump’s is counting down to November 2026, when American voters will decide whether to send Democrats to the House of Representatives, which could lay the groundwork for his impeachment.

The two leaders meeting today (14 May) need their summit to deliver stability. But there is an asymmetry to their domestic political horizons, with Xi preparing for a Congress 18 months away while Trump is bracing for an election in just six months’ time. This could be the most important factor underlying their face-to-face in the Chinese capital. In a way, everything else is choreography.

Xi, 72, requires external stability to manage a generational personnel turnover, the question of an unresolved succession, and a deflationary economy carrying up to $15tn in hidden local-government debt. Trump’s approval rating on inflation sits at 30%, and on tariffs, it is at 38%, with six special-election swings averaging 15 points toward the Democrats. Both men need positive achievements.

Neither can afford to stir a major US-China upheaval, so their summit will produce deliverables, but is unlikely to reset the bilateral relationship. That matters because Washington still sees big US-China meetings through the lens of the 1970s, when US President Richard Nixon and his chief envoy, Henry Kissinger, flew to China and set a template for great powers to trade strategic concessions. That template no longer applies. On offer in Beijing will be specific, nuanced bargains.

What they want

Xi’s priorities are domestic and sequential. The 15th Five-Year Plan, released this spring, will guide resource allocation through to 2030 and offer a legitimacy credential that Xi will carry into the 21st Party Congress. Its drafting coincides with Xi having to rebuild the top echelons of the People’s Liberation Army (PLA) and China’s diplomatic service simultaneously, after several high-profile figures were removed from power.

Personnel reconstitution on this scale cannot be conducted alongside a high-intensity external struggle, so Xi meets Trump seeking predictability, not escalation. Trump’s priorities are electoral and imminent. A Democratic House from November could reinstate impeachment prospects and shut down Trump’s legislative agenda for the second half of his four-year term.

With the Strait of Hormuz still closed and global oil prices still rising, Trump needs visible foreign-policy wins, not least to boost his voter-pleasing tariff and reindustrialisation agenda. He also needs energy prices to fall soon, while images of him at a state dinner and in the Great Hall of the People will, he hopes, show him looking statesmanlike. In short, for his White House team, this summit needs to be framed as a mid-term asset, rather than a contentious political showdown.

Beijing has the longer clock but not necessarily the stronger hand. Since Trump’s last state visit to Beijing in 2017, the US economic position has substantially strengthened relative to China’s. Trump will feel emboldened by that, but he must extract deliverables before he leaves, which he will. The question is: what is he willing to offer to Beijing?

Tariff threat

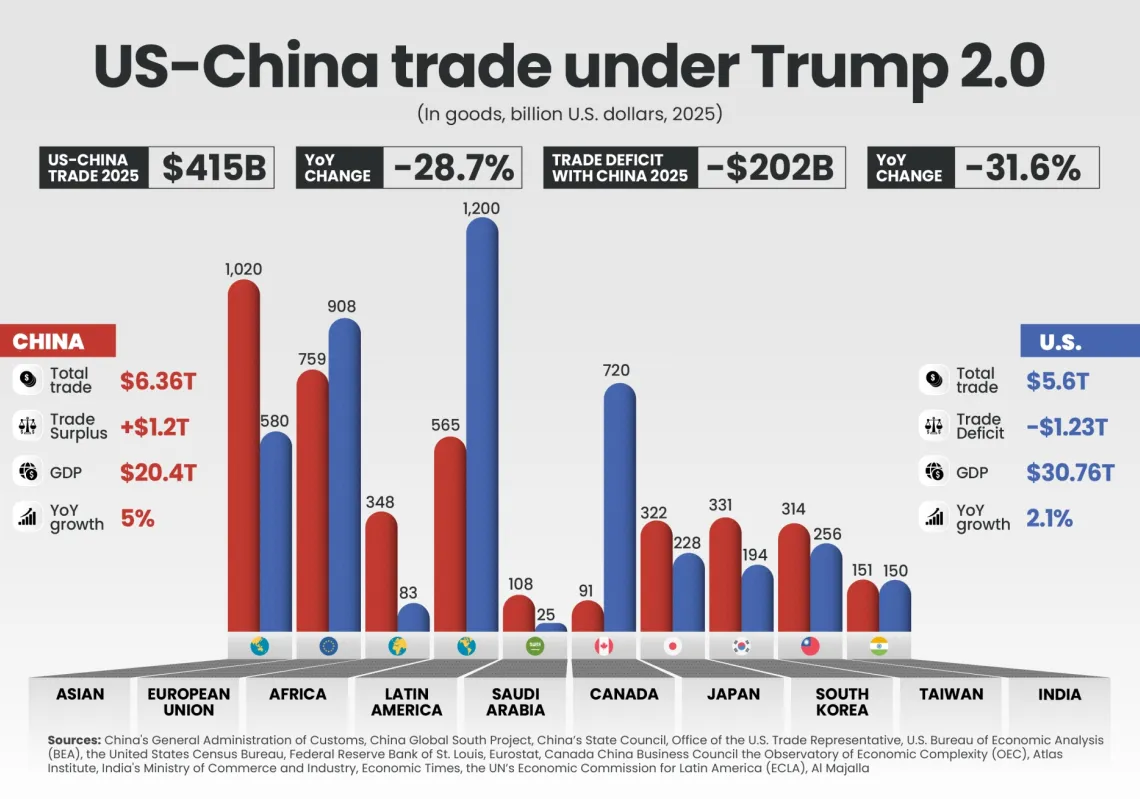

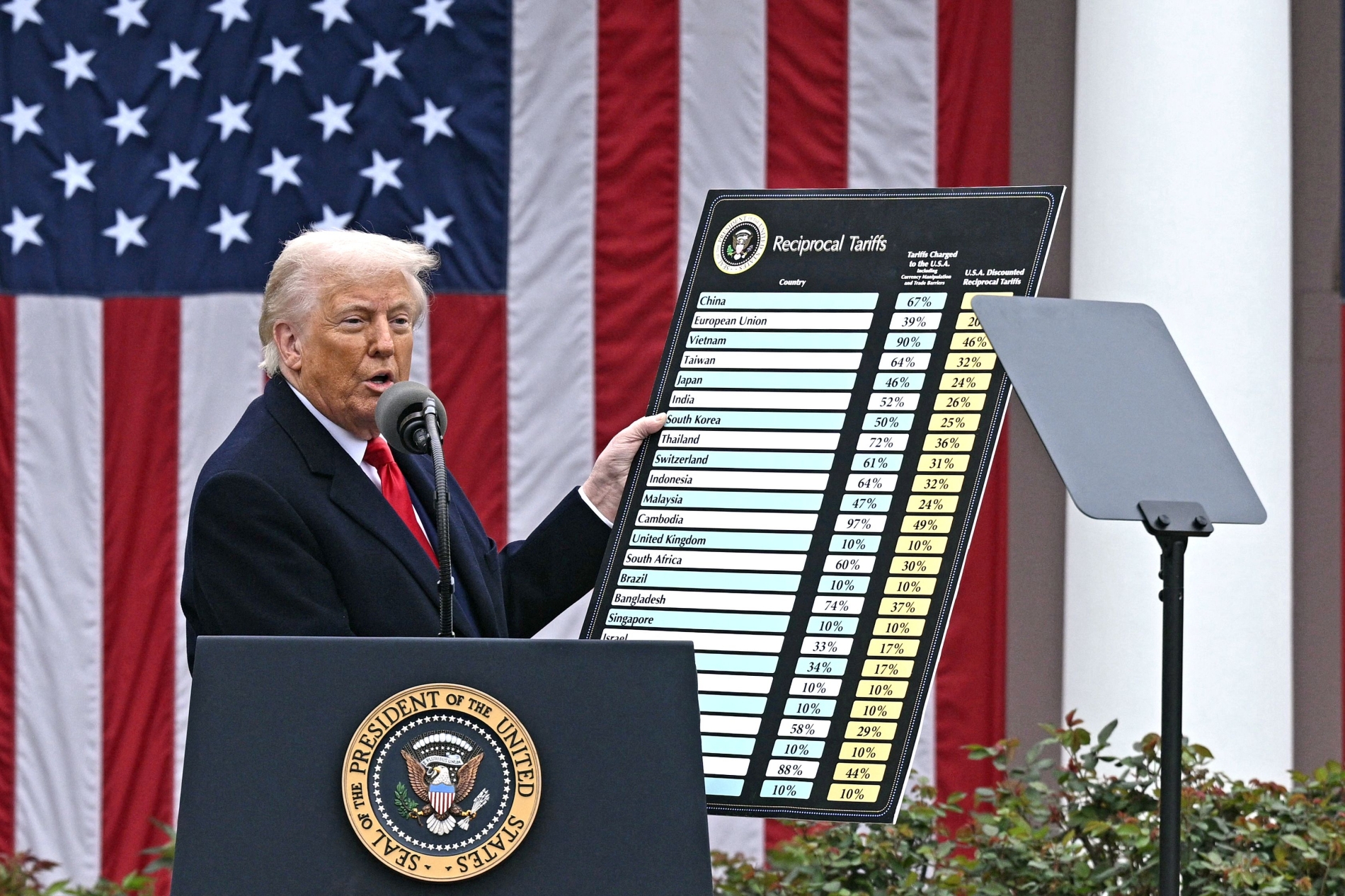

The single most consequential development since the trade truce in Busan in October 2025 is one that neither leader will openly mention in Beijing. On 20 February, the US Supreme Court ruled 6-3 that the International Emergency Economic Powers Act that Trump used to impose many of his tariffs does not authorise him to do so. This invalidated, for instance, the 10% fentanyl tariff and the 10% reciprocal tariff on Chinese goods, reducing the trade-weighted average tariff rate on China from 36.8% to 29.7%.

The ruling did not end everything. Section 301 duties from the first Trump term remain, as do Section 232 sectoral tariffs on steel, aluminium, vehicles, and semiconductors. But the China-specific top-up that gave Trump his negotiating leverage at Busan last year is gone, and the numbers are stark. Following the Supreme Court ruling, the trade-weighted average US tariff on all imports fell overnight, from 15.3% to 8.3%.

Trump responded by imposing a 10% global tariff under Section 122 of the Trade Act, but this is a diminishing asset. It is capped at 15%, expires after 150 days (unless Congress extends it), and, most importantly, cannot target China specifically. The administration has opened new Section 301 investigations into Chinese excess capacity, but this can take up to 12 months and requires evidentiary findings.

Trump, therefore, arrives in Beijing without the tariff threat that produced the Chinese concession, and his alternative instruments are far from apparent. By contrast, Xi’s negotiators arrived in Busan last year facing the possibility of 125% tariffs. Trump’s primary economic weapon has now been judicially disarmed, and his backup plan could take another nine months, so the situation is notably different. Few doubt that the threats will disappear, but they have been largely defanged.

In this climate, Beijing may not be as quick to offer rare-earth concessions as it was last year, or to provide ornamental relief without substantial US commitments. China knows that Washington needs the minerals it has for its most sensitive and strategic technologies, so export controls are important. Additionally, the White House will not want Beijing to initiate anti-monopoly proceedings against US firms. Meanwhile, the Blocking Rule invoked against US sanctions on Chinese oil refiners is still in focus.

The Iran inversion

The US-Israeli war on Iran, which led to Trump’s meeting with Xi being postponed earlier this year, is a foreign policy sore that has not yet healed. Iranian military retaliation against its attackers has effectively closed the Strait of Hormuz to commercial traffic, while the US Navy is intercepting tankers headed for Chinese ports in its own form of blockade, setting the stage for the biggest oil supply shock since 1973. As the world’s biggest oil importer, this will be near the top of Xi’s agenda.

Yet the Chinese president is no hostage to fortune here. Iran is a Chinese ally and one of its biggest sources of oil, yet it is also far from beaten, after six weeks of bombardment. Instead, it is Trump who feels the need to negotiate via Pakistan. Fuel prices at American forecourts could affect votes in November if he cannot reopen the strait soon. With his tariff sword sheathed, Iran no longer serves as his secondary leverage.

China is the diplomatic patron that Iran has historically leaned on. Beijing can offer Tehran what Moscow and others cannot: a guarantee of continued oil revenue at scale, settled outside the dollar system, and defiance of American sanctions through its newly invoked Blocking Rules. Chinese Foreign Minister Wang Yi received Iranian counterpart Abbas Araghchi in early May, shortly before China’s first-ever invocation of its 2021 Blocking Rules against US sanctions on five Chinese refiners.

China could leverage its influence with Tehran to support a phased reopening of Hormuz if the US lifts or narrows secondary sanctions on Chinese refiners, shipping insurers, and port operators dealing with Iranian crude. Beyond that, though, Trump and Xi are not expected to discuss Iran in detail, including its nuclear programme, war reparations, or Chinese arms transfers to Tehran.

Interests and positions

A functioning Strait of Hormuz is in Beijing’s national interest; nearly half its crude imports come from the Middle East. It is also in China’s interest that secondary sanctions on Chinese entities are conditional, not absolute. If Washington were to drop these, it would be strategically valuable to Beijing, perhaps more so than anything else.