Three weeks after the outbreak of the US-Israeli war on Iran, the world has entered an exceptionally dangerous phase. The confrontation has expanded far beyond the bounds of a conventional military conflict. It has developed into a multi-layered war in which military fronts converge with immense economic pressures, sending repercussions across the Middle East and deep into the global economy.

In this war, missiles are deployed alongside energy. Oil and gas markets, as well as trade and investment flows, are gripped by acute anxiety, and the economic burden is beginning to rival the direct costs of fighting on the battlefield. This is a war over energy and infrastructure, extending beyond attacks on oil and gas facilities to include strikes on essential assets such as desalination plants, ports, airports, and shipping lanes. With navigation through the Strait of Hormuz under threat and oil prices on the rise, the global economy stands at the brink of successive shocks from which few states are likely to be spared.

According to estimates, the Pentagon spent about $5.6bn on munitions during the first two days of the war, prompting Congressional concern over the rapid depletion of advanced weaponry stocks. To sustain the campaign, US President Donald Trump’s administration is expected to seek a supplemental defence budget that could run into tens of billions of dollars, despite possible opposition from some Democrats. Although the Pentagon has affirmed that it has the necessary capabilities, the likely duration of the war remains uncertain.

In the opening phase of the war, the campaign relied on expensive precision munitions such as Tomahawk missiles. It later shifted to cheaper laser-guided bombs once air superiority had been secured—a change that may reduce the cost of a single strike to less than $100,000. At the time of publication, US forces had targeted more than 5,000 sites in Iran. Meanwhile, Washington has redeployed advanced air defence systems such as THAAD and Patriot to the Middle East, a move experts warn could increase risks in other theatres, including the Indo-Pacific and Ukraine. Each interceptor costs about $4mn for a Patriot missile and $12.8mn for a single THAAD missile.

“The daily cost to the US military is estimated at $1bn,” said Riad Kahwaji, a geopolitical security analyst. “Israel’s daily military cost is also estimated at $320mn for the weapons and munitions used in attacks. The broader the military operations become, the higher the cost climbs.” What’s more, the deployment of additional forces carries vast financial consequences. “The arrival of a third American aircraft carrier means further funds must be committed to the war. The same applies to bringing in additional personnel for the conflict. This means that the cost to both states is rising steadily, quite apart from the economic repercussions.”

By the fourth day of the war, Kent Smetters, director of the Penn Wharton Budget Model at the University of Pennsylvania, estimated the economic cost of the conflict could reach $210bn. Direct costs, he said, would be between $40bn and $95bn, with a further $65bn for military operations and the replacement of equipment. He also projected an additional $115bn in economic losses resulting from disruptions to trade and energy. These figures did not include the additional $179bn associated with tariffs imposed under the International Emergency Economic Powers Act.

Initial US strikes used costly precision munitions such as the AGM-154 Joint Standoff Weapon ($578,000 to $836,000 each), alongside 20 systems from drones ($35,000 each) to multimillion-dollar missiles, plus 1,250 one-way drones ($43.8mn total). Aircraft carrier operations add a further $6.5mn to $13mn daily, with B-2 bombers at $130,000 to $150,000 per hour.

As the military campaign progressed, the Pentagon shifted towards cheaper munitions such as the Joint Direct Attack Munition, or JDAM. The cost of the smallest warhead of this type is about $1,000, while the guidance kit that turns conventional bombs into precision weapons costs around $38,000. The Pentagon later informed Congress that the cost of the war had exceeded $11.3bn in the first six days alone. Kevin Hassett, director of the National Economic Council and Trump’s senior economic adviser, also disclosed on 15 March that the war had so far cost at least $12bn.

Estimates by the Centre for Strategic and International Studies, however, point to a different picture. According to its analysis, the war’s cost could force the US administration to seek additional funding from Congress. Current figures do not include potential costs associated with replenishing Israeli equipment, rising military fuel prices, strengthening domestic security, and future obligations towards veterans.

Washington has also prepared a $20bn insurance programme to protect shipping in the Arabian Gulf and cover maritime losses through the US International Development Finance Corporation. In effect, it amounts to a form of political risk insurance combined with maritime financial and commercial guarantees, introduced after the disruption of oil and liquefied natural gas tanker traffic through the Strait of Hormuz.

Gulf-US investments

Amid mounting questions about Gulf investments overseas, a recent Forbes report noted that Gulf sovereign wealth funds hold about $2tn in US investments, accounting for more than 35% of their assets under management. These holdings are distributed across equities, bonds, and alternative investments such as real estate and infrastructure. More than 25% of these investments are allocated to equities, while 17% are channelled into fixed-income instruments, particularly US Treasury bonds.

Although Gulf investments in US equities amount to no more than about 1% of a $65tn market, their influence is more pronounced in private equity, where they stand at around $420bn, equivalent to eight to 10% of the market. Gulf states also hold roughly $307bn in US bonds, making the bond market a potential pressure point, since any sale of these holdings, or any decision not to roll them over, could push yields higher and raise borrowing costs in the US.

Gulf states have invested around $186bn in US alternative assets, particularly in artificial intelligence, technology, and real estate. Any retrenchment in these investments could affect start-up valuations, funding for artificial intelligence and clean energy, and segments of major property markets. In May 2025, Gulf states pledged substantial investments in the US, concentrated in energy, defence, and technology.

Energy choke point

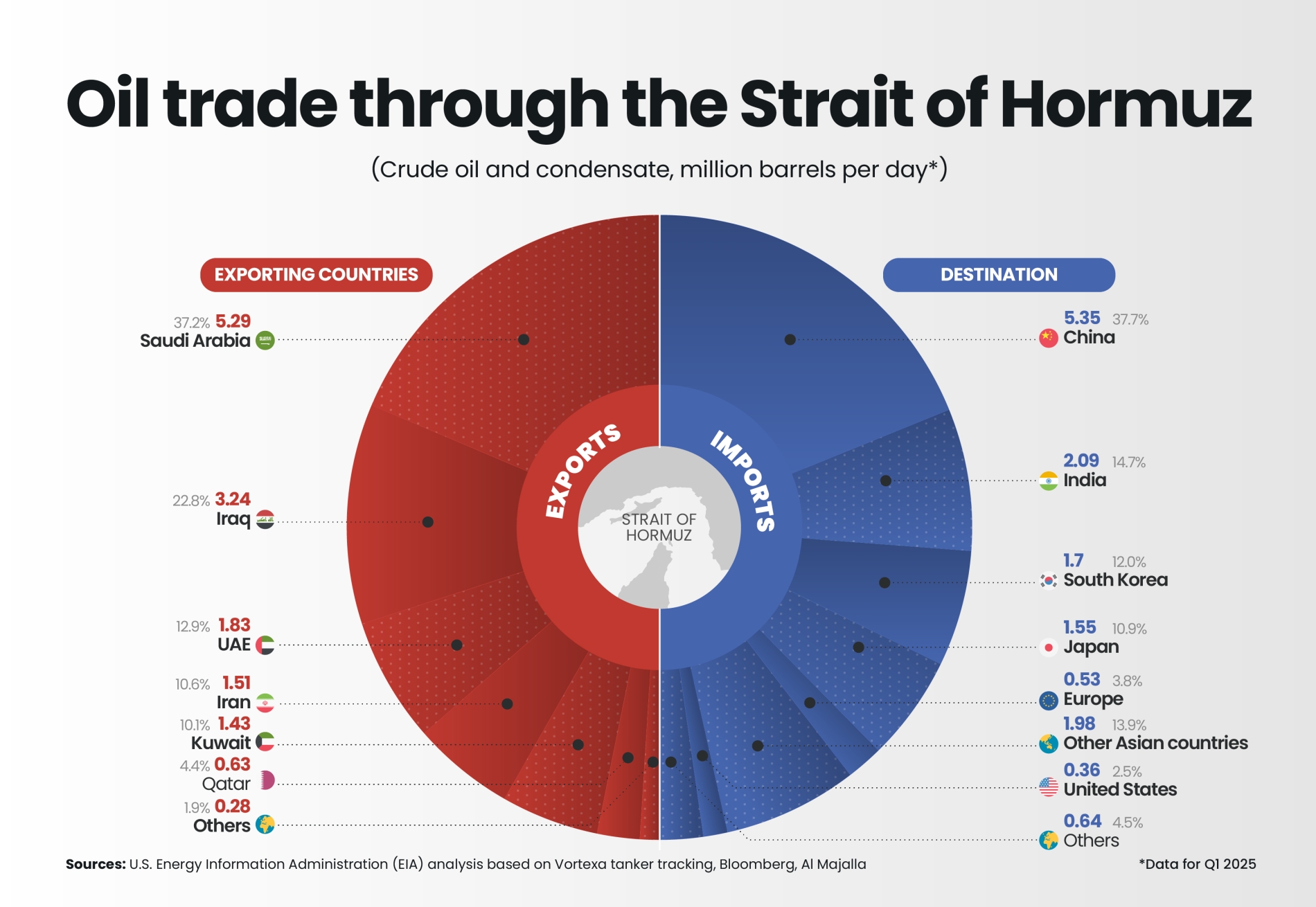

The Strait of Hormuz, meanwhile, now shapes global oil and gas prices and, with them, the course of the world economy. Within a week of the war’s opening salvos, Iran declared to Trump: “If you can bear oil rising above $200 a barrel, then continue this operation.” Iran is waging war against the global economy, wielding oil and gas as instruments of pressure, becoming both a pillar of the crisis and a gateway to its resolution. Few things reveal more clearly this war’s intimate bond between the military sphere and the economic realm.

Oil prices briefly surged to $120 a barrel, their highest level since 2022, prompting the UN to warn that any sustained rise in crude prices could unleash a fresh wave of cost-of-living pressures, echoing the crisis that followed Russia’s invasion of Ukraine in 2022. As of 19 March, Brent crude oil was trading around $109 to $112 per barrel.

Israeli losses

In the first week of the war, Israel’s Ministry of Finance said the economic losses resulting from the air war with Iran could exceed $2.93bn a week. That figure included restrictions on workplace access, school closures, and the call-up of reserve soldiers. For comparison, Israeli Finance Minister Bezalel Smotrich said last November that the cost of the war in Gaza had reached around $66bn, of which $5.5bn had been allocated to compensation payments.

According to Israeli business daily Calcalist, the restrictions imposed on the education system are causing losses of around $289mn a week. The mobilisation of reserve forces is generating a further loss of about $160.3mn. The army has called up nearly 100,000 reservists since the war began, at a time when half a million workers and employees have been absent from their jobs.

Indirect losses have also been felt across financial markets, in heightened stock market volatility and mounting pressure on the shekel, prompting some capital to temporarily retreat from the investment market. Experts have warned that the war could weigh on Israel’s credit rating, especially as the deficit widens and its financing becomes increasingly dependent on borrowing.

Economic analyst Sever Plocker has warned that the war could expose the Israeli economy to unprecedented risks and potentially push it into a prolonged recession. By contrast, JPMorgan Chase expects only a temporary slowdown followed by a swift recovery.

"The combined American-Israeli losses in the first days of the war amount to around $40bn in military terms alone," Mohammad Mousa, a professor of political economy, told Al Majalla. "The economic cost resulting from military losses and the continuation of the war, however, cannot be fully measured, because secondary losses accompany the military ones and approach $1bn a day. There are losses in tourism and in the aviation sector, affecting airlines and airports, in addition to rising oil prices and every form of insurance. The global economy will certainly be affected, and profoundly so."