In the decades since the Iran-Iraq War ended in 1988, Gulf energy strategy has been shaped by a simple premise: any closure of the Strait of Hormuz would be brief. Pipelines and terminals were built to cushion minor disruptions, but not to replace the route entirely. Yet Iran closed the strait in March, and it remained closed at the time of writing, so that premise is now under serious strain.

The US-Israeli war against Iran that began on 28 February and Iran’s subsequent retaliation across the Gulf have turned a long-recognised vulnerability into an operational emergency. What was once treated as a theoretical risk has become an immediate constraint, revealing the limits of the region’s alternatives. The infrastructure required to compensate for a sustained closure does not exist and cannot be built quickly or without risk.

The scramble for alternatives is now visible across the region. It is a story of engineering ambition meeting the hard limits imposed by cost, time and politics. Many of the routes now under discussion have been proposed before; others are new, shaped by shifting geopolitical alignments and the aftershocks of the Covid-19 pandemic of 2020 and the Russian invasion of Ukraine of 2022.

Yet even as interest in developing alternatives grows, the same constraints persist. New corridors are expensive, slow to deliver, and often politically contingent. More importantly, they remain exposed to the same security risks that now define the region. While diversification can reduce dependence on Hormuz, it cannot eliminate vulnerability. In practice, the security of Gulf exports will depend as much on diplomacy as on infrastructure.

Hormuz is one of the world’s most consequential passages, the narrow exit through which much of the Gulf’s oil, gas and commercial traffic must travel. It is both a commercial artery and a strategic lever. Until last month, it remained open. Its closure was a scenario analysts gamed out but never realised. Yet Iran’s response to being attacked was to use Hormuz as a weapon of retaliation. The Strait quickly morphed from notional risk to a live instrument of statecraft.

That is why the current crisis is so destabilising. As well as threatening barrels and tanker schedules, it calls into question the infrastructure assumptions that have underpinned Gulf energy planning for years. Planners have long assumed that if Hormuz were ever closed, the interruption would be short-lived, and enough backup capacity would be available to blunt the shock. Today, that assumption has been tested and found wanting.

Existing bypasses

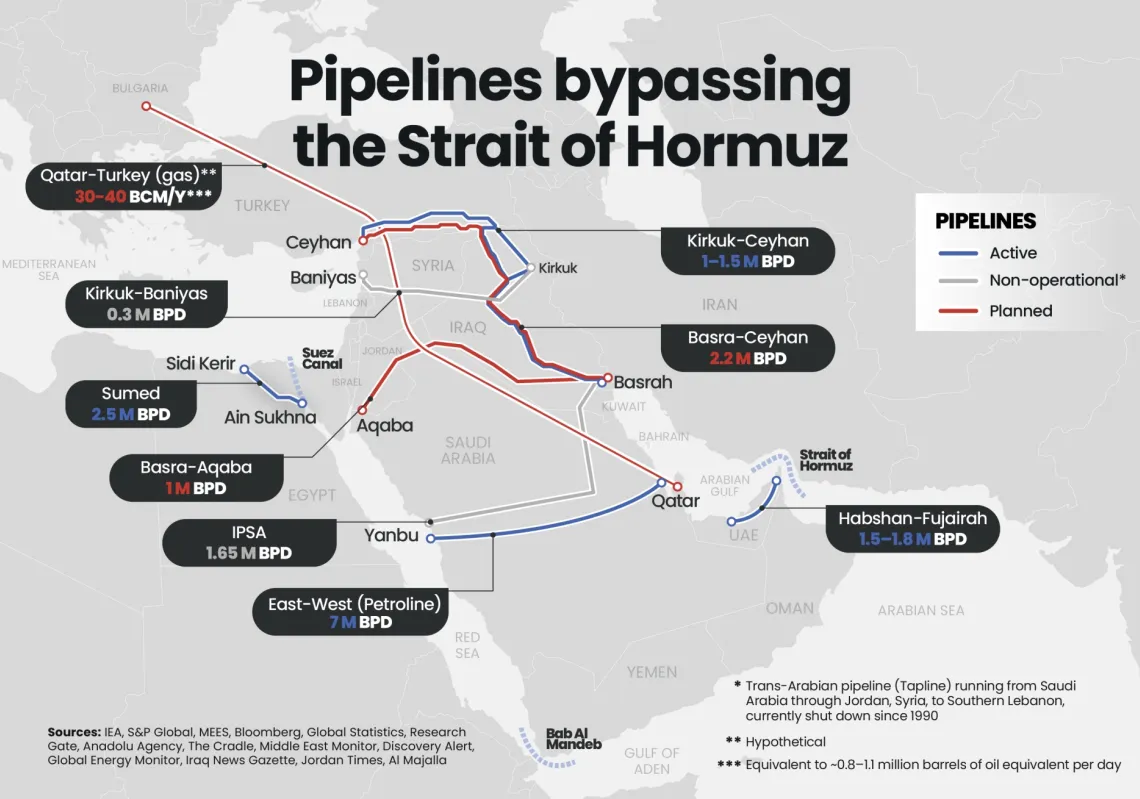

The Gulf has spent decades building workarounds, but most are partial, politically constrained, and vulnerable in their own right. While the system can be diversified, it cannot be fully insulated. This is most clearly demonstrated by the two functioning bypass pipelines in the Gulf: the East-West Crude Oil Pipeline (Petroline) in Saudi Arabia, and the UAE’s ADCOP pipeline.

Petroline is the older and larger one. Commissioned in the early 1980s during the Iran-Iraq War, it was conceived to develop western Saudi Arabia and later upgraded during the 1987 ‘Tanker Wars’ as insurance against any closure of Hormuz. The 1,200km system runs from the Abqaiq oil-processing centre on the Arabian Gulf coast westward to Yanbu on the Red Sea, sidestepping the strait entirely.

In March 2025, Saudi Aramco raised its capacity to seven million barrels per day (bpd). That proved prescient. When Hormuz was closed in early 2026, Aramco pivoted exports toward Yanbu and the East-West pipeline’s importance to global oil markets skyrocketed. The facility was targeted in Iranian strikes, resulting in a loss of around 700,000 bpd, but it has now resumed exports at full capacity. Even so, the terminal at Yanbu is now close to its loading limit, suggesting the bottleneck may lie not in the pipe but at its end.

The United Arab Emirates’ Abu Dhabi Crude Oil Pipeline, also known as ADCOP or the Habshan-Fujairah line, is smaller but was developed for a similar purpose. It was finally commissioned in 2012 after years of planning that accelerated during 2008-09, when concerns about Iran’s nuclear ambitions ran high. The 380km line runs from Habshan in Abu Dhabi’s interior through desert and mountain terrain to Fujairah on the Gulf of Oman, outside the Hormuz chokepoint. Its nameplate capacity is 1.5 million bpd, with room to rise toward 1.8 million bpd.

These two pipelines, Petroline and ADCOP, are the Gulf’s only operational crude bypass routes. Even at their theoretical maximum, they cover less than half of the normal Hormuz throughput. In practice, sustainable capacity is lower still, constrained by pumps, loading rates, and the obvious vulnerability of fixed infrastructure. Houthi drones struck Saudi pumping stations in 2019, forcing a temporary shutdown. In March 2026, drone attacks on Fujairah facilities disrupted loadings at the UAE terminus.

Menu of options

Even the most advanced bypass systems can only reduce exposure to shocks, not eliminate it, highlighting the limits of infrastructure as a substitute for stability. Beyond the two operational pipelines, the menu of alternatives to Hormuz includes corridors that once carried oil or were meant to, those that never fully developed into dependable substitutes, and those that were good in theory but not viable in practice, often for political or commercial reasons.

The Iraq Pipeline through Saudi Arabia, known as IPSA, is the clearest example. Built in the mid-1980s to give Iraq an export route outside the Arabian Gulf risk zone, it ran 1,650km from southern Iraqi oil fields to Yanbu, with a design capacity of 1.65 million bpd. It was closed in 1990 after Iraq’s invasion of Kuwait and has remained largely inactive since. Saudi Arabia seized the assets in 2001 in lieu of unpaid transit fees, and the line has been mothballed for a quarter of a century. A revival is discussed from time to time, but legal, diplomatic, and physical obstacles remain formidable.

The Kirkuk-Ceyhan pipeline tells a similar story. On paper, it should be a meaningful northern outlet for Iraqi crude, carrying oil from Kirkuk to the Turkish Mediterranean port of Ceyhan, bypassing the Gulf entirely. In reality, chronic disputes between Baghdad and the Kurdistan Regional Government over revenue-sharing and transit rights have repeatedly shut it down. A deal to restart flows was struck in March 2026, and the line has been reactivated, but initial flows are a fraction of the pipeline’s capacity and a reminder that political fragility can be as limiting as physical decay.

The older Iraq-Jordan pipeline belongs in the same category. It has been discussed for years as a way of giving Iraq an export route to Aqaba and the Red Sea, and the idea has been revived repeatedly in one form or another, but it has never become a dependable substitute for Hormuz. The problem is not the concept so much as the execution. The route would cross unstable political and security terrain, and it would still require major new capital, diplomatic coordination, and long lead times. It is attractive on paper because it redraws the map. On the ground, it remains a long-term possibility with risks, rather than an immediate fix.

These cases matter because they show that the problem is not just about building infrastructure; it is about keeping it alive amid shifting allegiances, competing interests, and recurring crises. A corridor that crosses several sovereign jurisdictions multiplies the chances of blockage. The more elaborate the route, the more opportunities there are for one party to hold it hostage. Alternatives can be proposed and built, but sustaining them depends on political conditions that cannot be engineered in the same way as infrastructure.

Read more: All you need to know about the India-Middle East-Europe Economic Corridor

Broader corridors

The search for alternatives has now widened beyond pipelines. Broader corridors, incorporating rail, road, pipelines, electricity, and data, are designed as systems capable of moving goods and energy without passing through a single maritime chokepoint. One of the more ambitious proposals is the India-Middle East-Europe Economic Corridor (IMEC).

Announced at the G20 summit in New Delhi in September 2023 by India, the United States, Saudi Arabia, the UAE, the European Union, France, Germany and Italy, IMEC is essentially a 21st-century Silk Road designed with 21st-century geopolitical goals. It proposes an Eastern Corridor linking India with the Gulf via existing shipping lanes, and a Northern Corridor running overland from the Gulf through Saudi Arabia, Jordan, and Israel to the Mediterranean port of Haifa, with onward links to Europe. It also promises to save time, which means money.