After years of missed economic opportunity, Syria’s oil reserves in the north-east are once again a strategic option for Damascus following a confluence of events, most recently the US-Israeli war against Iran and the latter’s decision to block the Strait of Hormuz, through which much of the Gulf’s oil and gas is exported.

The strait’s closure has disrupted global energy flows, leading the US and big energy importers to seek alternatives, knowing that shipping through the Bab al-Mandab Strait (to the Red Sea) could also be halted by Houthi attacks from Yemen. According to a document prepared by the US envoy Tom Barrack, a copy of which has been seen by Al Majalla, Syria forms part of the thinking.

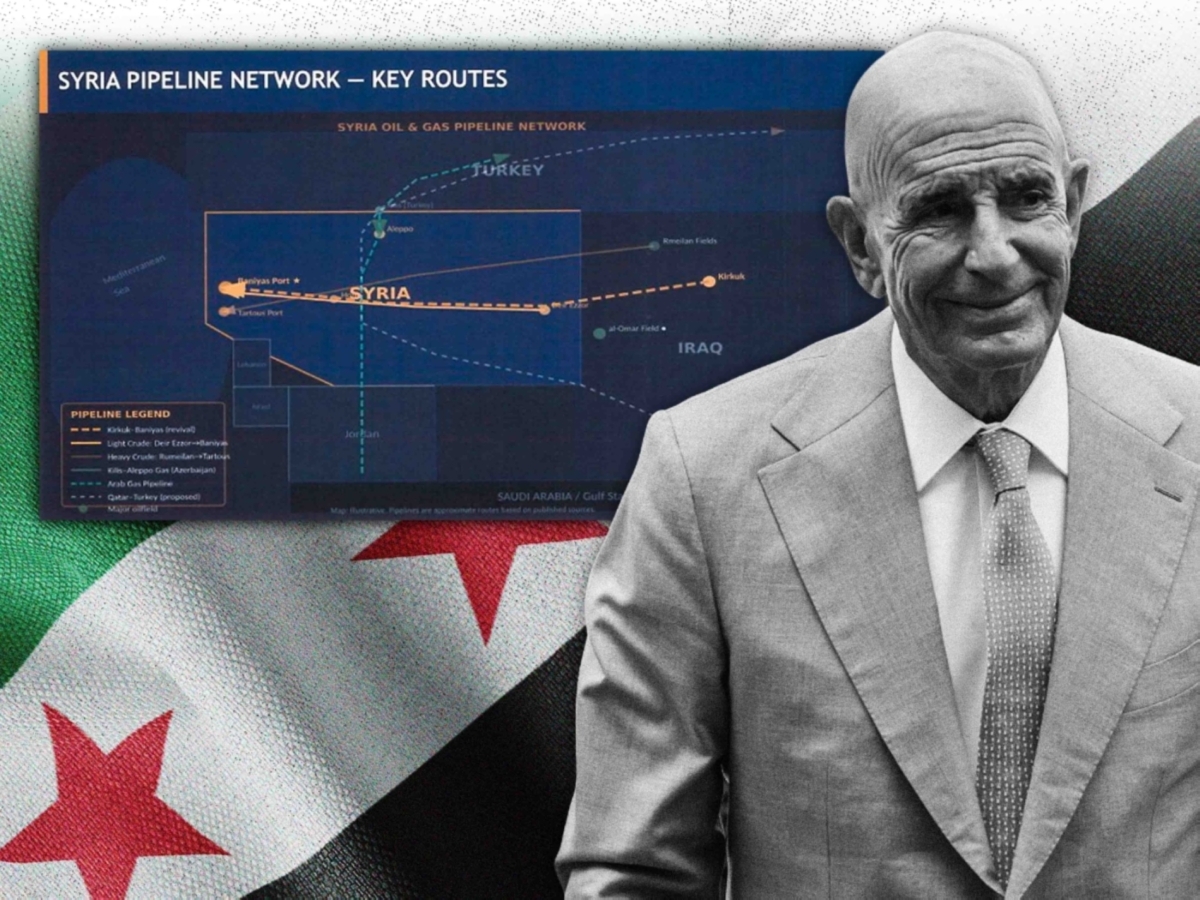

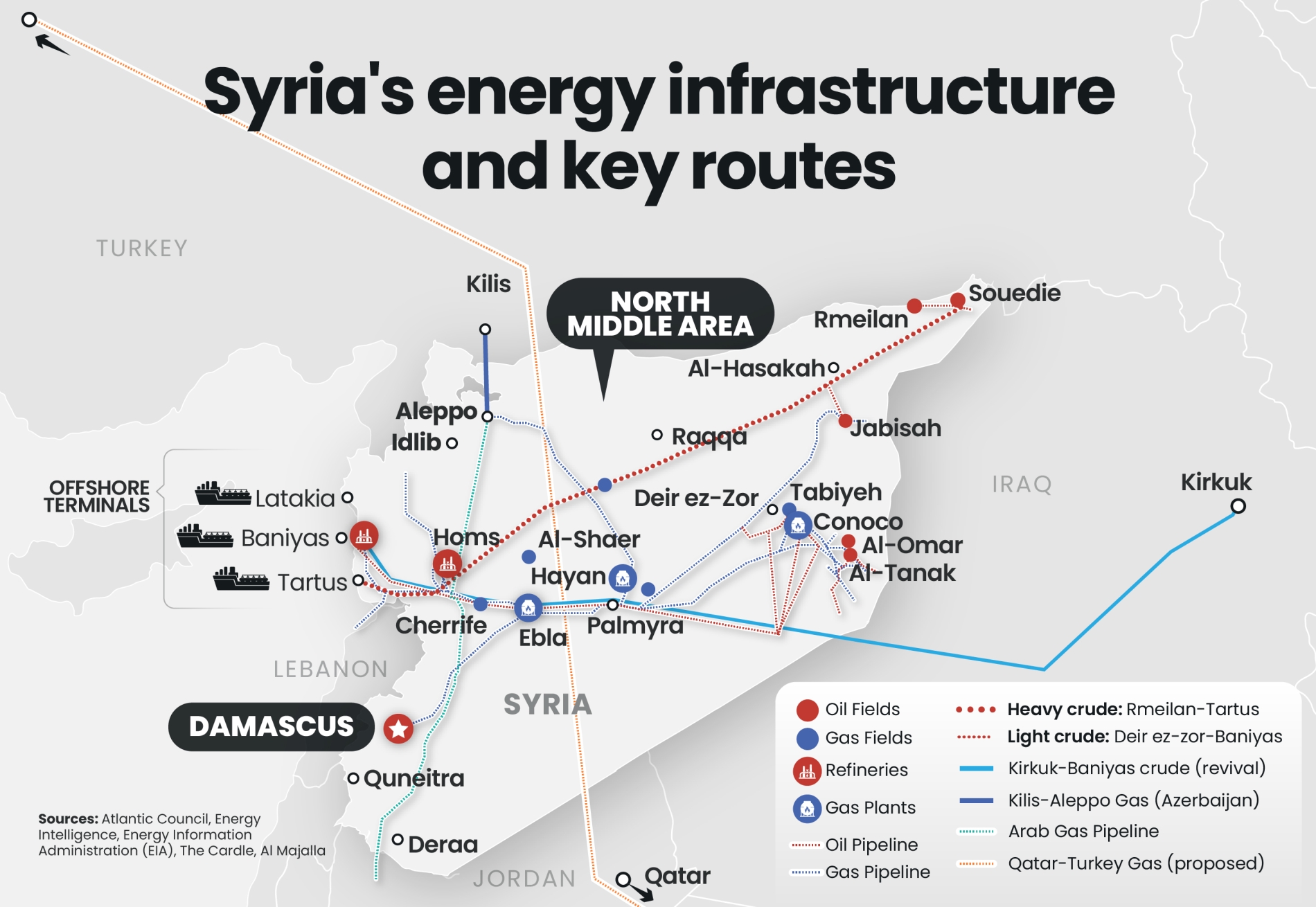

For all its complexities, Syria occupies a strategic geographic position that cannot be ignored. The ports of Baniyas and Tartus provide direct export access to the Mediterranean and Europe, while Syria offers the only viable overland route linking Iraq and the Gulf on one side with Türkiye and the European Union on the other. Could Syria become a major energy hub? After all, it would bypass Russian gas and compete with Israel’s ambitious energy corridors.

Promoting interest

The idea would once have been considered far-fetched, but several factors suggest that the moment may be ripe for different choices. Since the fall of Bashar al-Assad’s Syrian regime on 8 December 2024, efforts to rehabilitate the oil sector have accelerated. The Caesar Act (legislation outlining US sanctions against Syria) was repealed in December 2025, SWIFT (banking) transfers have now resumed, and the Syrian Petroleum Company (SPC) was re-established by presidential decree as a unified entity overseeing the entire value chain.

Last month, SPC participated in the CERAWeek energy conference in Houston, which is now open to international partnerships, particularly with US firms. Led by chief executive Youssef Qablawi, the firm showcased deep-water exploration projects to investors. In February 2026, SPC signed a memorandum of understanding with Chevron and Qatar’s Power International Holding to explore for oil and gas in Syrian territorial waters. Last week, it said Chevron had confirmed its intention to invest offshore, pending final contracts.

When it comes to Syria’s hydrocarbon resources, the timing is opportune. In January, Damascus finally regained on-the-ground control of the principal oilfields in the north-east from the semi-autonomous Kurdish-led Syria Democratic Forces (SDF), including Al-Omar, Conoco, Al-Tanak, Rmeilan, and Al-Suwaydiyah. This restored around 70% of Syria’s oil reserves to state authority after years of them being held by the SDF.

The government is open to resuming exports and welcoming back Western energy companies, supported by legislative reforms that allow full foreign ownership of projects and by Gulf investment pledges totalling $28bn. In February, Barrack said: “Syria is impressing us under the leadership of President Ahmad al-Sharaa.” He described the country’s political leadership as “a fundamental pillar in building a phase of recovery and stability”.

Signing deals

US firms Baker Hughes, Hunt Energy, and Argent LNG, alongside Saudi firms TAQA and ACWA Power, said in February that they were forming a consortium to explore for and produce oil and gas in north-eastern Syria, covering 4-5 exploratory sites.

More recently, on 5 April, SPC signed a contract with the Saudi company ADES covering the maintenance and development of existing wells, as well as the drilling of new exploratory wells, with gas production expected to rise by up to 25% within the first six months. Syria is also currently in talks with major international energy companies over licences for oil and gas exploration, amid estimates suggesting that undiscovered gas reserves may amount to trillions of cubic metres.

Late last year, SPC signed a memorandum of understanding with the American firms ConocoPhillips and Novatera to develop the gas sector and boost production from existing fields, alongside a similar memorandum with the UAE’s Dana Gas to redevelop and expand several strategic fields. Beyond that, SPC continues to discuss ideas with oil giants Eni and BP, while Damascus also appears open to Russian and Chinese investment, according to Qablawi.

The Syrian government expects public revenues to rise by around 149% in 2026, driven primarily by oil and gas income. Before the civil war began in 2011, Syria’s oil production peaked at 380,000 barrels per day (bpd), but conflict and damaged infrastructure led to it falling to around 110,000 bpd by 2026. The Syrian government estimates that total losses in the oil sector since 2011 amount to $115bn.

Reserves and output

Syria’s recoverable reserves are estimated at 2.5 billion barrels, with the potential to generate annual revenues of up to $6.1bn if the fields are brought back into operation. A 2010 study by the General Petroleum Corporation estimated Syria’s oil reserves at around 27 billion barrels and its gas reserves at 678 billion cubic metres, excluding offshore reserves.

Focusing on existing fields, output at Al-Tanak has fallen by 97.5%. The Conoco gas complex, which once produced 13 million cubic metres per day, has come to a complete standstill, while refining capacity in Homs and Baniyas has dropped from 250,000 bpd to 50,000 bpd. The pipeline network has sustained extensive damage, and only 37% of the country's electricity grid remains serviceable. More than 1,000km of the network in north-eastern Syria requires full replacement. Qablawi said it had “severely deteriorated as a result of chemical deposits and salts”.