If the Strait of Hormuz closure has exposed one reality, it is that Gulf states can no longer afford to depend on a single maritime passage. In that context, the Saudi port city of Yanbu may be emerging as the most realistic candidate to become a Gulf export hub on the Red Sea. Although it cannot fully replace Gulf ports, it is the only existing infrastructure in the Arab world capable of receiving vast volumes of oil from the east if the Strait remains effectively closed and traffic remains restricted.

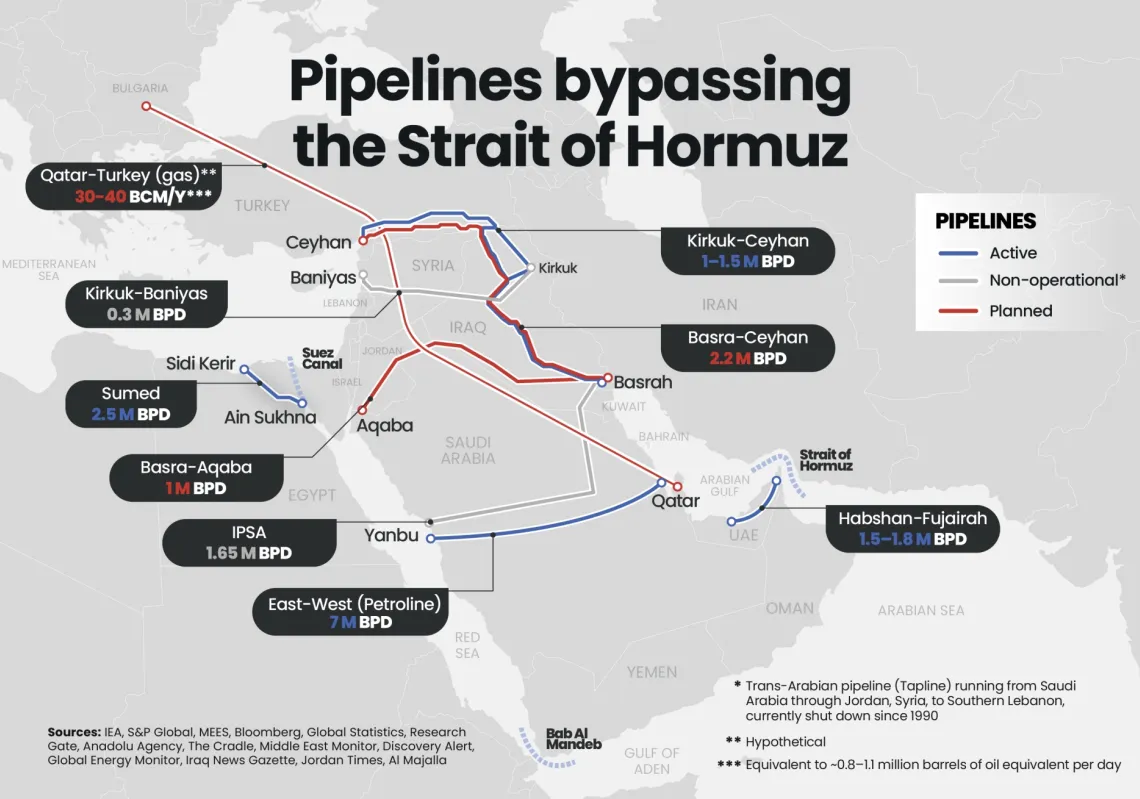

The logic is clear: Saudi Arabia has an overland oil corridor that can also be useful to other oil-exporting Gulf states. The East-West Pipeline, or Petroline, links Abqaiq to Yanbu across roughly 1,200km. Its capacity has been raised to 7 million barrels per day (bpd), according to recent Saudi statements. The International Energy Agency (IEA) says the sustainable flows, as historically tested, have been lower than that; however, the actual spare capacity available for rerouting stands at 3-5 million bpd, depending on operating conditions and export capacity on the western coast.

The gap between theoretical maximum capacity and practical throughput is the essential starting point for any serious discussion of Yanbu as a Gulf hub. Its importance rests on more than the pipeline alone. The city is a complete system, not merely a loading point. It contains oil export facilities, a vast industrial port, and the Yanbu refinery, which has a capacity of around 240,000 bpd according to official sources, alongside a relatively mature and integrated industrial and petrochemical base.

King Fahd Industrial Port in Yanbu also has an annual handling capacity of 210 million tonnes, according to official Saudi data. That gives the city an advantage that extends beyond crude shipments to refined products, petrochemicals, and the industrial supply chains linked to them.

The US-Israeli war on Iran and Tehran's retaliation over recent weeks have focused minds. Shipping data reported by Reuters showed that crude exports from Yanbu surged in March 2026 to nearly 4 million bpd, after which loadings remained at elevated levels. Other data put the port’s export capacity at around 5 million bpd. On 9 March, the IEA also recorded a daily high of 5.9 million bpd from Saudi ports on the western coast, compared with an average of 1.7 million bpd in 2025.

These figures don't mean that Yanbu is ready to absorb the export burden of the entire Gulf, but they do show that the market has already tested a westward shift in flows, and that the system proved capable of absorbing a substantial part of the shock. As such, one of Yanbu’s three strategic advantages is existing readiness. Other Gulf states seeking an alternative to Hormuz would build on a Saudi pipeline already in operation, including ports, refineries, storage facilities, and operational experience.

The second advantage is Yanbu’s geographical position. The Red Sea opens directly onto the Suez Canal, Europe, and the Mediterranean. It also offers access to Africa, while exports bound for Asia can still move south through Bab al-Mandab. Its third advantage is sovereign stability. The entire corridor lies within a single state until it reaches the sea. Projects that span several countries are exposed to political risks in each country, not to mention border disputes between states.

'Saudi safety valve'

Turning Yanbu from a ‘Saudi safety valve’ into a Gulf export hub means expanding the corridors that feed into it. The existing line primarily serves Saudi Arabia, and part of its capacity is already absorbed by refineries and facilities in the west. Any Gulf-wide scenario would require new parallel lines within Saudi Arabia leading to Yanbu, or networks linking Kuwait, Bahrain, and perhaps the eastern areas adjacent to Qatar to the main Saudi network, followed by an expansion of pumping, storage, and port capacity on the western coast. But the IEA has warned that the logistics and supply chains required to reroute such large volumes have yet to be rigorously tested.