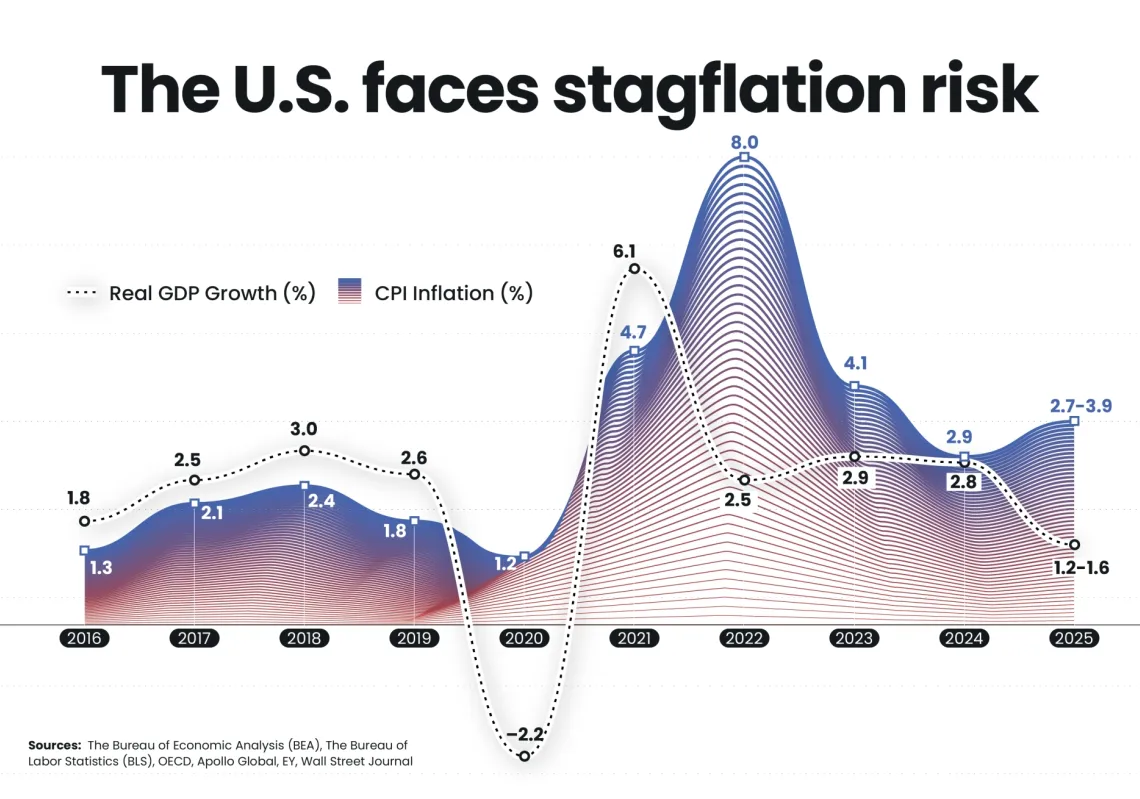

Since Donald Trump took office in January last year, America’s economy has continued to be the envy of the world. In 2025, while Britain, France and Japan eked out annual GDP growth of around 1%, and Germany all but stood still, American output grew by 2.1%. In the past 15 months, American stock markets have broken record after record. And all this even as the president has unleashed seemingly anti-growth policies like mass deportations of migrant workers and chaotic trade wars.

Observers who had predicted economic disaster are left scratching their heads. Perhaps, some now whisper, the policies are not as destructive as economists had assumed. Others wonder what might have been. For all its strength, America’s economy could, on this interpretation, be doing even better. But how much better? Put another way: how big is the “MAGA tax”?

One way to arrive at a figure is to imagine what America’s economy would look like in this levy’s absence. Mr Trump inherited an economy that was growing strongly. It has since had three boosts, which The Economist has roughly quantified.

First, the artificial-intelligence boom. Capital expenditure by just four AI-giants—Alphabet, Amazon, Meta and Microsoft—topped $350bn in 2025 and should hit roughly $700bn in 2026.

The binge has unleashed a wave of spending on data centres, chips, cooling systems and software. In 2025, real investment in information-processing equipment, software and data centres grew by more than 15%. In gross terms, this surge contributed nearly one percentage point to annualised GDP growth, accounting for about half of the economy’s expansion.

This figure, though, overstates AI’s true contribution to growth. Roughly two-thirds of data-centre spending is on equipment, much of it imported from Asian manufacturers like South Korea and Taiwan. When American firms buy this, most of the economic activity occurs abroad. To estimate how much the spending contributes to American GDP, we subtracted the rise in imports of real equipment from the surge in AI investment. By our reckoning, around $50bn of the AI-investment boom in 2025 reflected additional domestic production, adding 0.2 percentage points to annualised GDP growth.

The AI frenzy has also fuelled America's stockmarket, the source of the second boost to growth. Between Mr Trump’s election and the end of 2025, the S&P 500 index of large American firms rocketed by 15% in real terms—unusually fast by historical standards. That added $5tn more to household wealth than would have accrued in a typical year. Americans tend to spend a small share of such windfalls. Still, using a conservative rule of thumb that each dollar of equity wealth raises spending by two cents in the first year, this probably raised consumption by $100bn in 2025, or 0.5% of total consumer spending. Given shoppers’ central role in America’s economy, the wealth effect may have added 0.3 percentage points to growth.