Will the US-Israeli war on Iran disrupt global food supplies and send the prices of grains and other staples soaring? This is a question on the lips of many as concerns intensify over possible interruptions to the supply of chemical fertilisers. Such disruptions could depress agricultural output in food-producing nations, weakening their ability to meet global consumer demand.

This prospect revives memories of the turmoil that followed the Ukraine war, which disrupted grain shipments from the then fifth-largest exporter and tightened global supplies, with the impact felt most keenly in Asia and Africa, particularly in Egypt, one of the world’s largest wheat importers.

According to Philipp Schiebe, executive director of the German Federation of Agricultural and Food Industries, conditions strikingly similar to those of February 2022 are re-emerging, as nitrogen fertiliser prices on the global market draw ever closer to the highs recorded at the outset of the Russia-Ukraine war.

The current war involving the US, Israel, and Iran has already had a profound effect on oil and gas supplies. Around 20 to 25% of global crude oil flows (about 20 million barrels) pass through the vulnerable Strait of Hormuz, along with one-fifth of global liquefied natural gas trade. The conflict has also shaken the fertiliser trade, nearly 30% of which moves through the same narrow passage.

Gas is a core input in the production of nitrogen-based fertilisers such as urea and ammonia. A report published by the British energy agency Argus Media in June 2025 noted that any closure of the Strait of Hormuz could disrupt global trade in fertilisers and their raw materials by 20 to 50%, exposing importing countries to the gravest risks.

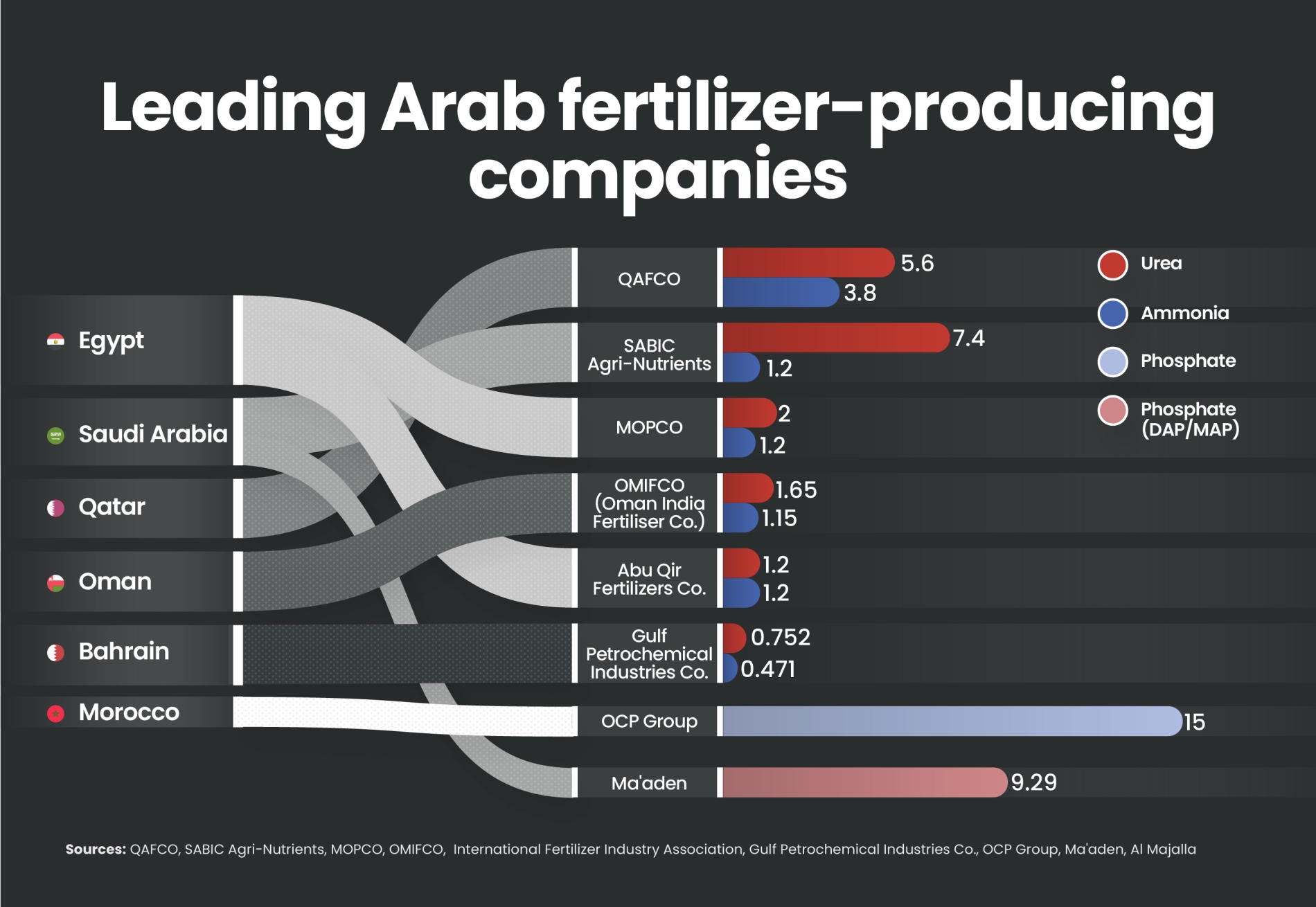

The Gulf states remain a key source of these materials, supplying around half of the global seaborne sulphur trade, one-third of the global urea trade, and one-fifth of the global ammonia trade.

Major markets such as China, India, and Brazil depend heavily on these supplies, leaving them vulnerable to any disruption. The danger extends to phosphates—especially Saudi exports—while the sulphuric acid market remains fragile and already burdened by scarcity. The report also notes that any interruption to Gulf flows could create severe bottlenecks in global supply chains and trigger sharp price rises, with immediate consequences for global food security.

Surging prices

Since the outbreak of war, prices for key fertiliser products have surged. Urea prices in the Middle East climbed above $590 per metric tonne, a 19% rise in less than a week, reaching $690 on 27 March. Diammonium phosphate prices on the US Gulf Coast also rose to $655 per tonne, gaining more than $30 per tonne, or about 5%. Bank of America has warned that the US-Israeli war on Iran threatens between 65 and 70% of global urea supplies, while prices have climbed by between 30 and 40%.

Although fertiliser prices remain well below the record highs seen in late 2021 and early 2022, these increases come at a moment when farmers across the world are already grappling with weaker prices for grains, oilseeds, and other field crops. Higher fertiliser costs shrink producers' profit margins and may prompt some to scale back fertiliser use, with unavoidable repercussions for both yield and quality.

The immediate effect may remain relatively contained, since many farmers have already secured agricultural inputs for the spring season in the northern hemisphere. However, if the conflict persists, it could begin to shape planting decisions and productivity in the southern hemisphere, while also affecting fertiliser use in rice cultivation across South and Southeast Asia.

Unlike fuel, fertilisers are not supported by global strategic stockpiles, leaving some countries more vulnerable than others. Latin America—more distant from the direct fallout of the war and home to Brazil and Argentina, major powers in both energy and agriculture—appears to be in a relatively safer position. Even so, Brazil's agriculture minister, Carlos Fávaro, has warned that the country could face difficulties in fertiliser supplies.

Following attacks on liquefied natural gas facilities in Ras Laffan and the suspension of gas output, QatarEnergy has halted production at the world's largest urea plant. Egypt, which accounts for about 8% of global urea trade, may face difficulties producing nitrogen fertilisers after Israel declared force majeure on gas supplies to the country.

In India, three urea plants have cut production following a sharp drop in liquefied natural gas supplies from Qatar. India, home to nearly one-fifth of the world's population, depends on the Middle East for more than 40% of its urea and phosphate fertiliser requirements. Bangladesh, meanwhile, has shut down four of its five fertiliser plants, while the Australian company Wesfarmers has warned of possible delays to shipments, including urea. Farmers in the US are also confronting supply shortages, with the country facing an estimated 25% deficit in fertiliser supplies.