The joint US-Israeli attack on Iran has triggered retaliatory strikes, with Tehran hitting back at Israeli and American assets throughout the region. The global energy market has already experienced a pronounced shock from war-related disruptions. In a region where energy exports underpin fiscal stability, even the perception of prolonged instability can reverberate through markets from Asia to Europe.

About 20% of the global supply of oil passes through the Strait of Hormuz. As such, any closure of the geopolitical chokepoint has severe ramifications. With Iran’s Islamic Revolutionary Guard Corps prohibiting the passage of vessels, the strait is effectively closed, despite US President Donald Trump’s assertion that the US Navy could begin escorting oil tankers through the strait.

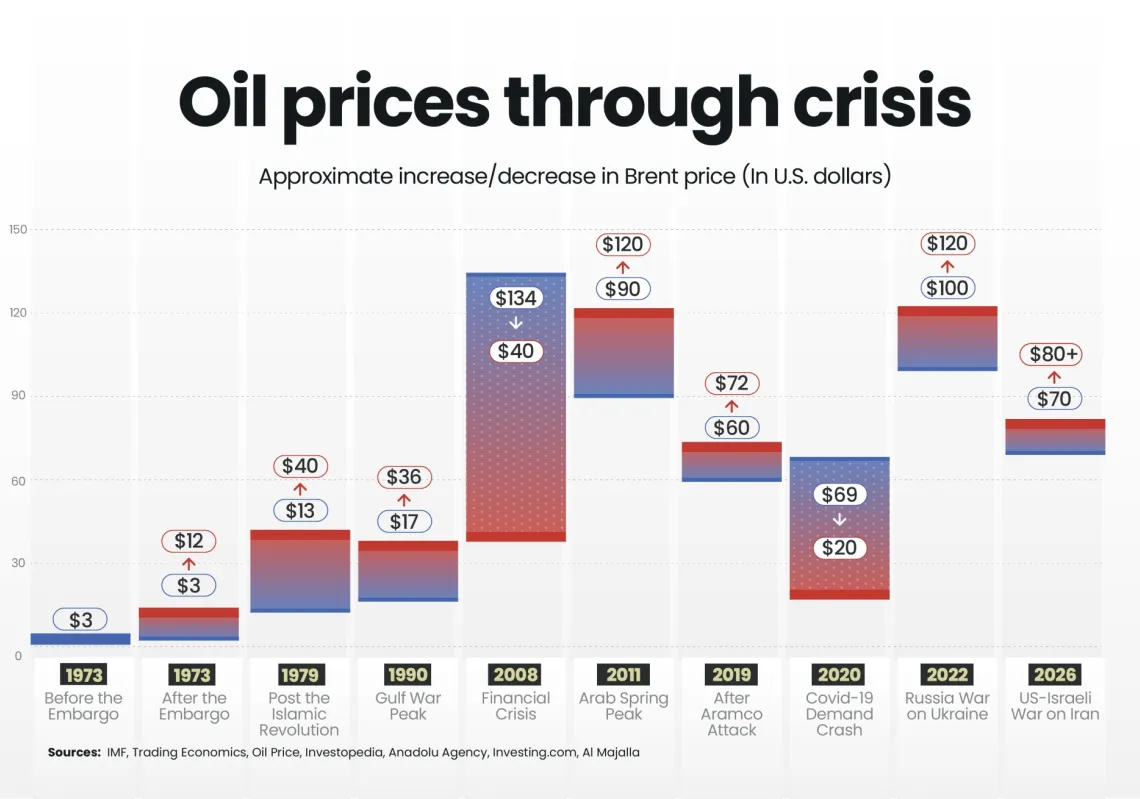

The most pessimistic scenario suggests any closure of the strait, even a limited one, could drive oil prices to around $130 a barrel. That outcome is unlikely, but the prospect alone is enough to unsettle traders and investors.

When US and Israeli military operations began on 28 February, Brent crude was trading at $72 a barrel. By 4 March, it had risen to $82 a barrel amid intensifying regional hostilities, including Iranian attacks on both oil and liquified natural gas (LNG) facilities in Saudi Arabia and Qatar, respectively. On 2 March, Qatar suspended LNG production, leading to a spike in gas prices. Qatar is among the world’s largest exporters of natural gas.

On 1 March, in an attempt to absorb the shocks caused by the war, OPEC+ members—including Saudi Arabia, Russia, Iraq, the UAE, Kuwait, Kazakhstan, Algeria, and Oman—agreed to raise oil production by 206,000 barrels a day from April, amid warnings that crude oil supplies could be disrupted.

However, analysis by Canada's Royal Bank of Commerce has noted that OPEC+ production hikes are likely to have a limited impact, given that most member states are already operating at their effective maximum capacity, except Saudi Arabia.

Fears are also mounting that further Iranian strikes could hit additional oil and gas facilities across the Gulf, damaging infrastructure and disrupting supplies. Oil remains central to the region's economic model, and any open-ended interruption to supplies could strain financial conditions across the Gulf.

A blow to diversification

Apart from exposing the structural vulnerability of Gulf energy flows, the war has also threatened ambitious Gulf plans to diversify their economies away from oil dependency and to strengthen non-oil sectors such as tourism and financial services. They have revised laws and regulations governing economic activity, improving the investment climate and attracting foreign capital.