Since Russia’s invasion of Ukraine, Europe has had to rebuild its energy and trade networks for the decades ahead. Until the continent can rely on renewables, part of the answer will come from natural gas in the eastern Mediterranean. For the states with claims in this region of the sea, the question is longer simply about discovering new gas fields or securing export contracts, but who will Europe get its gas from.

European energy security has come to mean much more than replacing Russian gas with supplies from elsewhere. States are redesigning a broader network that encompasses gas, ports, electricity grids, hydrogen, data and supply chains. Within this framework, two distinct models have emerged. On the one hand, Türkiye is seeking to become a regional centre for energy trading, while on the other, Israel is pursuing a partnership via gas exports, electricity links, technology, and infrastructure. The outcome of this contest will also affect Egypt and the Gulf states, as well as the future of trade corridors and clean-energy projects across the region.

Leaving Russia

Before its invasion of Ukraine in 2022, Russia was the continent’s largest external supplier, selling the European Union (EU) around 45% of its natural gas imports—around 155 billion cubic metres (bcm) per year, according to the European Commission. Most Russian gas arrived via pipeline networks through Belarus, Ukraine, and Türkiye, or through Nord Stream 1, which directly connected Russia and Germany.

The collapse of this model prompted the EU to launch its ‘REPowerEU’ plan in May 2022. This sought to reduce dependence on Russian energy, diversify suppliers, increase imports of liquefied natural gas (LNG), and accelerate the shift towards renewables. Russia’s share of EU gas imports fell from 45% to 19%, but rose again in 2024, so the Commission introduced a new roadmap designed to end dependence on Russian energy altogether while accelerating the transition to cleaner sources.

Under the plan, each member state was required to prepare, by the end of 2025, a national strategy for phasing out imports of Russian gas, oil and nuclear fuel, with Russian gas imports ending by the end of 2027. It bans new contracts, terminates spot contracts by the end of 2025, and tightens oversight of Russian gas trading. It also targets Russia’s ‘shadow fleet’ of vessels used by Moscow to evade oil sanctions, and restricts contracts involving Russian uranium and other nuclear materials. Legislation is now being prepared to make the roadmap binding.

Figures from the Council of the European Union show that Norway became the bloc’s largest gas supplier in 2025, accounting for 30.9% of imports. The United States followed with 26.2%, while North Africa (including Algeria and Libya) supplied 12.7%. Azerbaijan accounted for 3.9% and Qatar for 3.7%. The variation shows how Brussels has diversified its energy supplies since 2022.

Yet Europe expects more from its energy partners than the ability to export gas; it wants investment in infrastructure, energy corridors, green hydrogen, and closer links between energy and commercial markets. This is reflected in the EU’s Global Gateway strategy, launched in 2021 to strengthen international partnerships through investments of up to €300bn in infrastructure projects worldwide covering energy, transport, digitalisation, health, education and scientific research.

The International Energy Agency (IEA) advises that states diversify their sources of supply, make their electricity grids more resilient, speed up the development of low-emissions hydrogen, and modernise energy infrastructure. Together, these changes are intended to support a more flexible and sustainable energy system.

Two different models

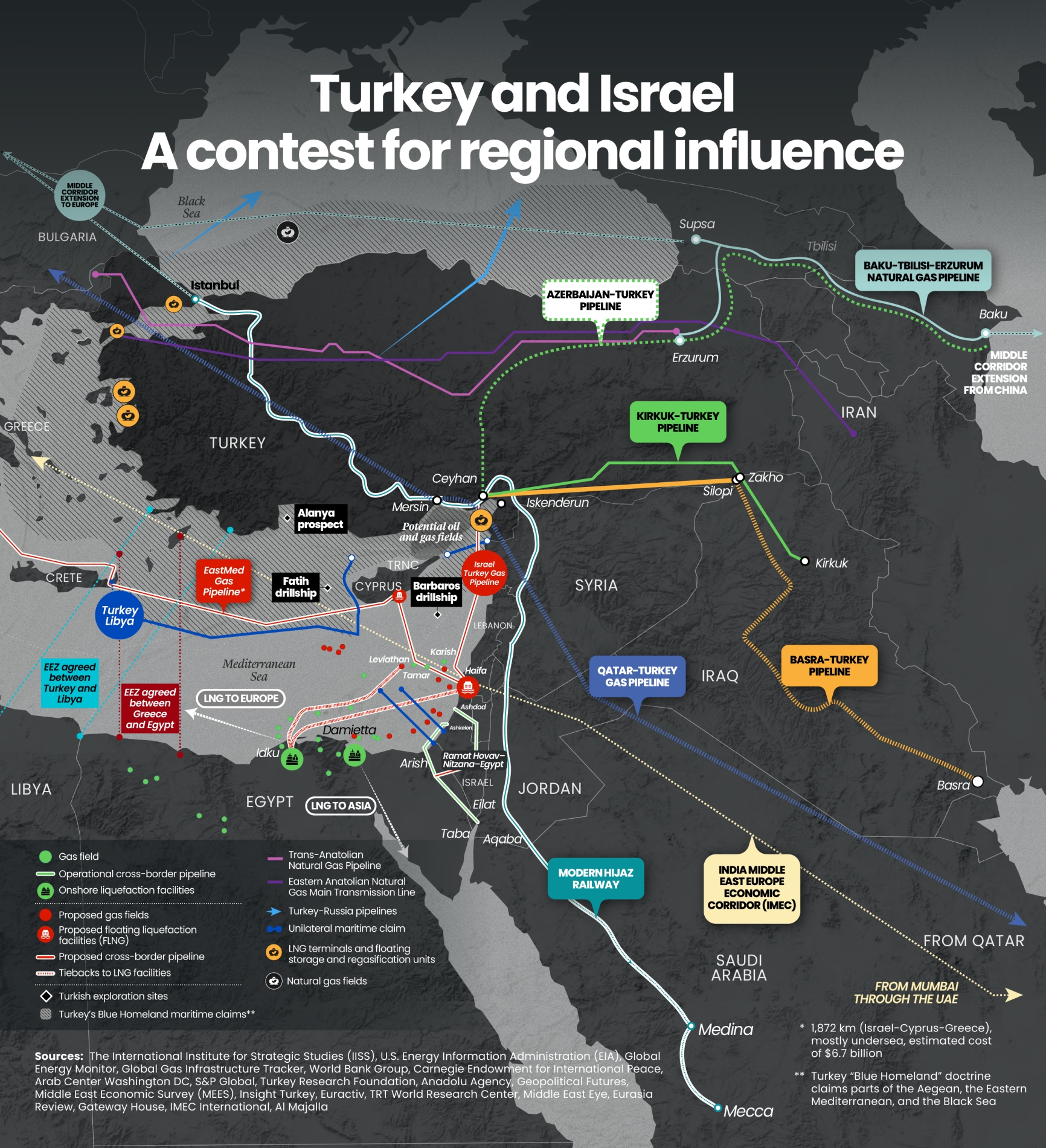

Türkiye and Israel matter because they offer Europe two very different models. Türkiye, which lies between Russia, Azerbaijan, Iran, the Middle East and Europe, thinks geography means that it can transform itself from a transit country into a regional centre for energy trading. It already has one of the region’s most sophisticated gas transmission networks, and the Turkish Straits play an important role globally—the Turkish Foreign Ministry says 3% of global oil demand passes through them.

The Trans-Anatolian Natural Gas Pipeline, known as TANAP, carries Azerbaijani gas and forms the backbone of the Southern Gas Corridor. Its current annual capacity is around 16bcm, about 40% of which is allocated to the Turkish market, with the rest carried to Europe through the Trans Adriatic Pipeline, or TAP. Plans are under way to increase TANAP’s annual capacity to 31bcm. Parallel proposals would raise TAP’s capacity to 20bcm, almost doubling the current volume.

TurkStream consists of two parallel pipelines, each with an annual capacity of 15.75bcm. One serves the Turkish market, the other sends gas to southern and central Europe. Türkiye also has advanced LNG infrastructure, including two onshore terminals, three floating storage and regasification units, and underground storage facilities. Together, these assets allow it to receive gas from several sources and direct it either into the domestic network or onwards to regional markets.

Its combined LNG regasification capacity is 51.3bcm per year, equivalent to around 40 million tonnes, which puts Türkiye second in Europe after Spain. The infrastructure enables Ankara to diversify its gas imports, maintain stable domestic supplies, and redirect volumes towards neighbouring markets. Türkiye’s ambitions go well beyond transit, however.

Reforms for success

Ankara wants to establish a regional gas trading platform where supplies from several sources are pooled, traded, and re-exported, as they are in Europe’s major gas hubs. President Recep Tayyip Erdoğan set this objective in 2023, and Energy Minister Alparslan Bayraktar similarly spoke of turning Türkiye into “a major regional gas hub”.

Its advantages include geography, its existing infrastructure, and its proximity to energy sources in Russia, the Caspian basin, the Middle East and the eastern Mediterranean. Success nevertheless depends on further gas-market reform, more diverse supplies, less reliance on any single provider, and greater transparency and liquidity. The IEA and the European Commission regard these conditions as essential to any successful regional gas trading hub.