SpaceX IPO: an astronomical bet on Musk’s space visionhttps://en.majalla.com/node/331440/science-technology/spacex-ipo-astronomical-bet-musk%E2%80%99s-space-vision

SpaceX is getting ready for a stock market debut that could be the biggest IPO in history. Yet investors will not be investing only in rockets and launches. What Elon Musk is offering is closer to a sweeping wager on the future of space itself: reusable rockets, satellite internet, artificial intelligence, orbital data centres, and long-term promises of a sustained return to the Moon and a route towards Mars.

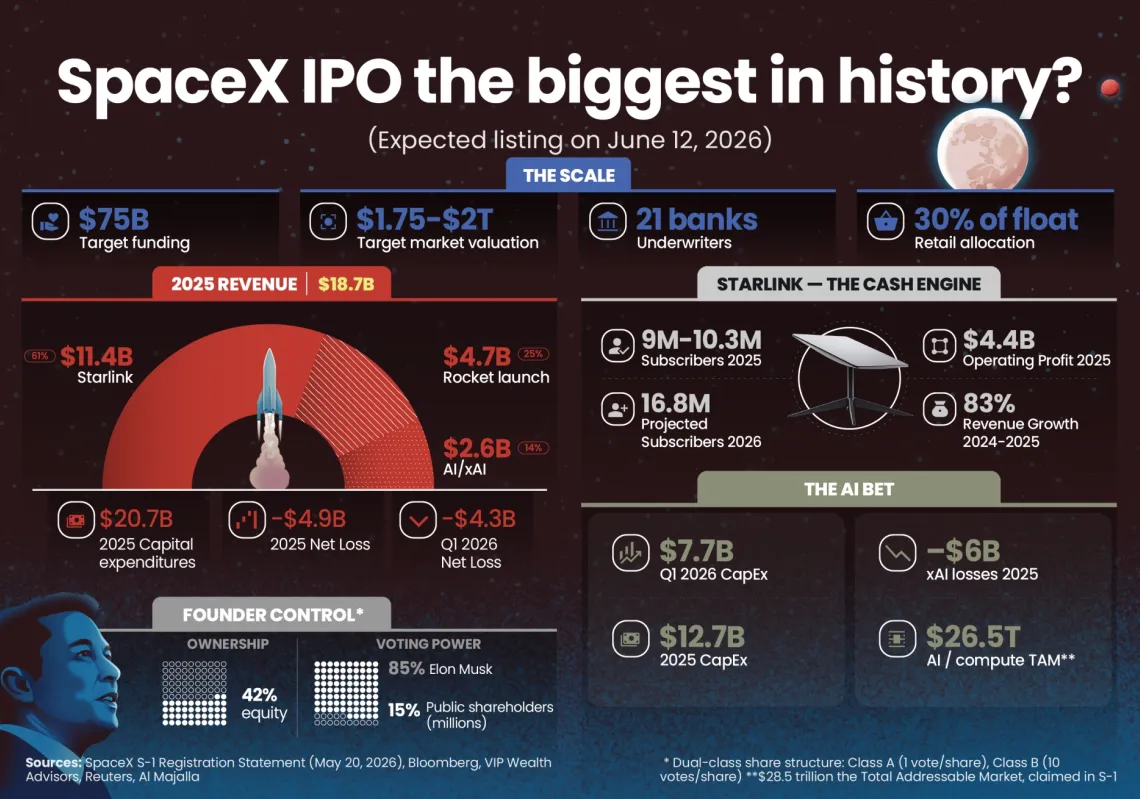

According to reports, the company plans to offer roughly 555.6 million shares at $135 each, in a deal that could raise as much as $75bn and give SpaceX a valuation approaching $1.75tn. If the deal proceeds on these terms, the offering would be more than a landmark technology listing. It would mark a defining moment in the evolution of the space industry, accelerating its shift from a sector reliant on government funding and defence contracts into the heart of public markets. There, investors would become direct participants in financing the infrastructure of a new space age.

Yet the expected offering does not appear to be following the conventional script. Companies preparing to go public typically announce an initial price range, allowing them to gauge investor demand during the roadshow before setting a final price based on the weight of that demand.

SpaceX, by contrast, appears to be moving towards a fixed price before meeting investors, an unusual step that reflects Musk’s familiar style. He does not wait for the market to shape the narrative. He prefers to shape the narrative himself.

Astronomical growth

In less than two decades, SpaceX has evolved from a private venture in one of the world’s most complex industries into a pillar of the American space programme. The company emerged amid serious engineering and financial doubts before transforming the sector through reusable rockets. At first, the idea seemed little more than a gamble: a rocket would carry its payload into orbit, then return its first stage to Earth for landing and reuse. What initially appeared to be a technical spectacle became an economic model that rewrote the rules of the launch market.

With that transformation, SpaceX no longer sells a ‘rocket’ in the traditional sense. It sells access to orbit. Falcon 9, with its high launch cadence and reusable design, has made reaching orbit a more routine and less scarce service than it was in an era dominated by governments and major defence contractors. With each successful flight, the company has come to resemble a space transport operator rather than a traditional rocket contractor.

If Starship carries the wager on the future, Starlink is the more mature asset already in motion

This new rhythm is what led NASA to place increasing trust in SpaceX for some of its most sensitive missions. Through the Commercial Crew Program, the company restored astronaut launches from American soil to the International Space Station (ISS) using the Crew Dragon spacecraft and Falcon 9 rocket, ending years of reliance on Russia's Soyuz vehicles following the retirement of the Space Shuttle. NASA's relationship with SpaceX therefore evolved beyond the purchase of launch services into an operational dependence on a private company to transport humans into space.

This dependence is even clearer in the programme to return to the Moon. NASA selected SpaceX to develop the Starship-based human landing system, intended to carry Artemis astronauts from lunar orbit to the Moon's surface and back again. This is no minor element of the programme but one of its most complex and demanding components. Moving safely from lunar orbit to the Moon's surface and then returning requires a powerful and highly reliable system, placing SpaceX at the centre of America's ambition to establish a sustained presence on the Moon.

SpaceX does not appear to need capital as a form of rescue. It is far removed from the profile of a fledgling enterprise searching for a final chance to survive. The company possesses contracts, influence, and operational infrastructure that few rivals can match. What Musk is asking the market to finance is a much larger transition: from a business that reshaped the launch market to one seeking to command the routes of transport, communication, and work beyond Earth.

Starship took off from Star Base in Boca Chica, Texas, for its sixth flight test on 19 November 2024.

Sky-high ambitions

At the centre of this transition stands Starship. Falcon 9 gave SpaceX its edge, yet it is not enough for Musk's larger ambition. He does not merely want to launch satellites or carry astronauts to the ISS. He wants a rocket capable of lifting vast amounts of equipment into orbit, supporting the lunar programme, and eventually opening the way to Mars. Starship, in this sense, is more than a new rocket. It is an attempt to create a heavy-lift workhorse for space, one that could, if successful, transform the economics of launch once again.

Yet developing Starship is a costly and risk-laden process. Every test can reveal challenges in engines, control systems, landing, reusability, or endurance across the full flight profile. The objective is not a single successful launch but the transformation of heavy-lift spaceflight into a repeatable and dependable service. This distinction is crucial, because an economy on the Moon or Mars cannot be built on a symbolic mission. It requires a sustained capacity to move people, equipment, fuel, and infrastructure.

The financial figures reveal the scale of the challenge. SpaceX recorded revenue of around $18.7bn in 2025, yet swung to a net loss of nearly $4.94bn after posting a profit the previous year. In the first quarter, revenue rose to around $4.69bn, while losses widened further. This equation leaves investors facing a clear question: do these losses represent the cost of building the infrastructure of the future, or are they a warning that the company's valuation has raced years ahead of its economic reality?

If Starship carries the wager on the future, Starlink is the more mature asset already in motion. Conceived as a space-based internet network for areas poorly served by terrestrial infrastructure, it has acquired the weight of a strategic asset. It now serves homes, remote regions, ships, aircraft, and disaster zones, and could prove decisive in conflict environments where ground communications networks collapse or come under attack.

Starlink's importance to SpaceX lies in the way it combines revenue with influence. Each new satellite expands coverage, increases capacity, attracts more users, and creates further opportunities for contracts with companies, governments, and militaries. Most importantly, SpaceX does not depend on another company to launch its satellites. It owns the rocket, owns the network, and sells the service. This closed loop gives it a rare advantage: the rocket serves Starlink; Starlink provides cash flow and political influence; those returns help finance Starship; and Starship may one day launch larger numbers of satellites and heavier equipment.

Starlink executives are exploring whether a licence could be granted in Lebanon, but talks may have slowed in the country's political and legal morass.

For this reason, the story of the IPO is not confined to rockets or spaceflight. SpaceX is trying to persuade the market that it is building a new layer of infrastructure: communications, orbital transport, future computing capacity, and services that could become part of American national security. With its merger with xAI, and amid growing discussion of computing resources for artificial intelligence and even solar-powered data centres in space, the company appears to its supporters as a point of convergence between space, artificial intelligence, and communications.

This vision, however, creates a profound difficulty in valuation. With a valuation approaching $1.75tn and revenue of around $18.7bn, the company would trade at an exceptionally high price-to-revenue multiple. It cannot be assessed easily on the basis of profits, since it has recorded losses. Much of its valuation therefore rests on future expectations rather than established financial results. Investors are not buying present earnings so much as the possibility that SpaceX will become the foundational infrastructure of a far larger space economy.

Musk is offering investors a place inside a story that begins with Falcon 9 and Starlink, passes through Starship and the Moon, and extends towards Mars

Eye on Mars

In Musk's narrative, the Moon is not the end of the road. True, the Artemis programme gives SpaceX a central role in America's return to the lunar surface, yet the more distant objective remains Mars. For him, the Moon serves as a testing ground for technologies, operations, and the ability to transport equipment and human beings beyond Earth's orbit. If SpaceX succeeds in establishing regular transport services around Earth and to the Moon, talk of Mars will seem less fanciful, even if it remains strewn with immense technical, financial, biological, and political obstacles.

Here, Musk's existential narrative comes into view. When he speaks of ensuring that humanity does not meet the fate of the dinosaurs, he is not addressing investors in the language of a conventional chief financial officer, but in that of a historical mission. The premise is that a civilisation confined to a single planet remains vulnerable to catastrophe, whereas the ability to live beyond Earth gives humanity a greater chance of survival. The notion may strike many as remote, even inflated, yet it plays a crucial role in SpaceX's investment narrative: it gives the company the aura of a civilisational project, not merely a financial asset.

Image of an astronaut on Mars.

Larger sell

This narrative allows Musk to sell something larger than a balance sheet or a valuation multiple. He asks the market to view current losses as the cost of construction, failed tests as stages of learning, and rockets that sometimes explode as part of the long journey towards a new space infrastructure.

He succeeded with this approach before at Tesla, persuading investors that a loss-making company surrounded by serious doubts could become a symbol of transformation in the automotive industry. Today, he is attempting to apply the same logic to SpaceX on a far larger stage.

Despite the strength of the narrative, the IPO carries difficult questions. The first is that a significant part of SpaceX's value rests on projects whose economics have yet to be proven: Starship as a platform for repeated heavy-lift launches, data centres in space, a vast expansion into artificial intelligence, and a lunar or Martian economy that remains in its theoretical infancy. The second is the company's heavy dependence on Musk himself, given his record of challenging entire industries and the controversies and governance risks that accompany him.

The expected ownership structure reinforces this point. Musk will retain substantial voting power through shares with enhanced voting rights, keeping strategic decisions in the hands of the founder and a limited circle of insiders. For supporters of SpaceX, this arrangement safeguards the company's long-term vision and shields it from the pressures of short-term quarterly results. For sceptics, however, it means committing enormous sums to a company where they will have no real influence over decisions.

The complications deepen because of the overlap among Musk's companies. The relationships among SpaceX, xAI, and Tesla raise questions about shared interests, related-party dealings, resource allocation, and capital direction. Some may view this overlap as an integrated system in which each part reinforces the others, while others may see it as a potential source of conflicts of interest and opacity.

Assistance is being provided to NASA astronaut Butch Wilmore to exit SpaceX's Dragon spacecraft after it splashed down in the water off the coast of Tallahassee, Florida.

Increased competition

Musk is not moving in a vacuum. SpaceX may hold an advanced position, but rivals such as Blue Origin are seeking to establish a larger presence in heavy-lift launch and lunar projects. Other companies are also entering NASA's expanding ecosystem, developing everything from lunar vehicles to robotics, power systems, and landing technologies. Washington, meanwhile, has little interest in relying entirely on a single company, even one that currently leads the field. Space has become a sensitive domain of national security, and supplier diversity is no longer a luxury. It is a strategic necessity.

For this reason, SpaceX's IPO is more than a financial event. It signals a new phase in the financing of America's space ambitions. If the offering succeeds, it will suggest that Wall Street is prepared to finance part of the future infrastructure of space, and that investors are willing to pay a high price for a stake in a company that may become an almost unavoidable gateway to orbit, the Moon, and perhaps Mars. If the offering faces resistance or requires revised terms, it will serve as a reminder that the market, however fascinated by Musk, still asks about profitability, valuation, control, and execution risk.

In the end, Musk is trying to turn SpaceX's IPO into a moment larger than the sale of shares. He is offering investors a place inside a story that begins with Falcon 9 and Starlink, passes through Starship and the Moon, and extends towards Mars and perhaps an entire space economy. Yet the question that will decide the market's response is not whether the story is compelling. It clearly is. The question is whether it deserves one of the highest valuations in the world before its grand promises become sustainable profits.