The United Nations Development Programme is supporting the Kuwaiti government in deploying debt instruments to help finance development in education, healthcare, and clean energy. Those debt instruments include sovereign bonds and sukuk (sharia-compliant) bonds, now that Kuwait can access diversified financing channels thanks to the enactment of a new public debt law, which authorises government borrowing of around $97.5bn, with maturities extending to 50 years.

The aim is to let the state manage fiscal deficits from lower oil prices and non-oil revenue vulnerabilities. Although Kuwait has a sovereign wealth fund with $1tn in assets, the Future Generations Reserve Law keeps those resources out of bounds for debt financing, instead mandating the reinvestment of returns to preserve national wealth for future generations.

States and their IOUs

Sovereign borrowing has long formed part of the fiscal landscape of modern states, and some governments have accumulated substantial obligations. For them, debt servicing can impose heavy burdens and leave some countries on the brink of insolvency and default if fiscal governance is weak and spending is unchecked, particularly on defence or projects of limited productive value.

Further drains of state resources can include sprawling administration and urban overexpansion, yet sovereign borrowing can be a catalyst for constructive transformation when directed towards productive development. States that use debt to improve healthcare, education, and infrastructure, for instance, usually raise overall living standards.

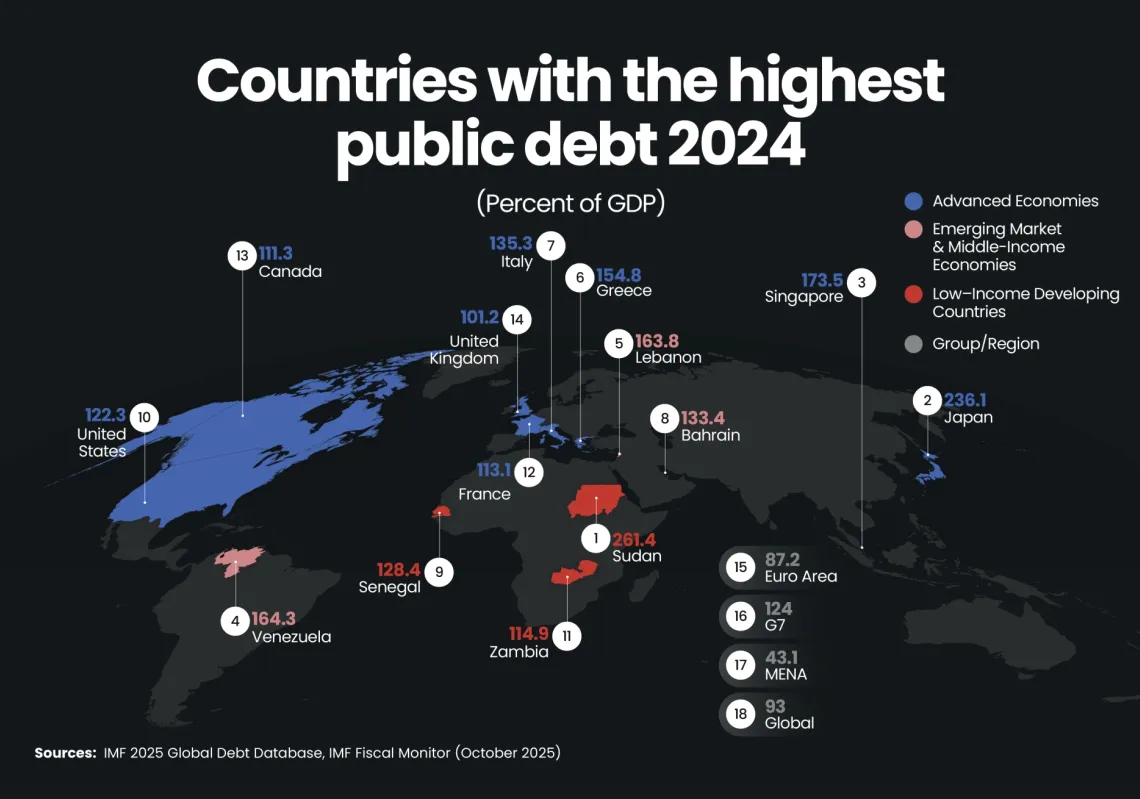

Japan offers a striking example. By March 2025, its sovereign debt had reached a colossal $8.4tn, with 88% held domestically (the Bank of Japan and insurers are among the biggest creditors). This was around 235% of gross domestic product (GDP) in 2024, a burden stemming from the 1991 financial market collapse, when government intervention became necessary.

Saudi Arabia is the leading sovereign debt issuer in the Gulf, accounting for roughly 44.8% of total issuance. The United Arab Emirates follows with 29.9%, with Qatar issuing 12.8%, and Bahrain, Oman, and Kuwait making up the rest. Saudi public debt has now reached around $390bn. The borrowing reflects the scale of projects pursued under Vision 2030, spanning infrastructure, tourism, education, health, and sustainability.

Such initiatives have strengthened core public assets and reinforced Saudi Arabia's economic position within the G20. The UAE maintains a comparable debt-to-GDP ratio, while Kuwait has entered the borrowing cycle over the past year, as lower oil prices add pressure to budgets.

Projections from the International Monetary Fund (IMF) show Saudi and Kuwaiti debt growing over the next few years, while the debt of the UAE, Qatar, and Oman is projected to fall. In 2024, total Saudi government debt was 26.2% of GDP, and in 2025 it was 29.2%, rising to 31.8% in 2026 and 40.7% by 2030. In Kuwait, it was just 2.9% of GDP in 2024, 7.3% in 2025, 10.7% in 2026, and is expected to be 24.5% by 2030.